Executive Summary

Three shifts. One window. Same conclusion.

Puerto Rico raises its rate on new applicants in seven months.

01.

Act 38-2026 extends Act 60 through 2055 but moves the rate on capital gains, dividends, and interest for new Individual Resident Investor decree applicants from 0% to 4% on January 1, 2027. The 0% rate is preserved for applications filed before the deadline.

Singapore has closed its offshore licensing loophole.

02.

FSMA Part 9 took effect June 30, 2025. Singapore-based Digital Token Service Providers serving only overseas customers now require an MAS licence — and MAS has stated it will generally not issue one. Affected operators must restructure into Singapore or wind down.

The UAE has unified federal and Dubai-level oversight.

03.

The August 2025 CMA–VARA cooperation agreement establishes mutual recognition of VASP licences and a shared enforcement framework. The result: the world's most fully codified virtual-asset regime — with 0% personal income and capital gains tax retained.

Read the full brief

17-page PDF research report · May 2026 Edition · sourced to primary regulators

Download PDFThe Three Shifts

The map of where crypto wealth lives is being redrawn around it.

Three independent regulatory moves — one a hard deadline, one already in force, one structurally consolidated — converging into a single conclusion for every operator, advisor, and brand in the category.

i.Shift 01 · The Hard DeadlinePuerto Rico Act 38-2026: the 0% window closes.

The most consequential regulatory deadline crypto wealth has faced at scale. The current 0% rate on capital gains for new Individual Resident Investor decree applicants ends on January 1, 2027 — replaced by a 4% rate under the new law.

Puerto Rico's Act 60-2019 has been the single most powerful legal structure available to U.S.-citizen crypto investors. Under IRC §933, bona fide residents of Puerto Rico exclude PR-sourced income from federal tax. Under Chapter 2 of Act 60, qualifying residents pay 0% on capital gains accrued after residency, including gains on cryptocurrency acquired post-move. For an investor with $5 million in unrealized gains, the difference between selling on the mainland and selling under an Act 60 decree is in the seven-figure range.

Act 38-2026 — enacted earlier this year — extends the program through 2055 but resets the rate for new applicants. Applications filed on or after January 1, 2027 will be subject to a 4% preferential rate on capital gains, dividends, and interest instead of the current zero. Existing decree holders keep their original terms; new applicants who file before the deadline also lock in 0% under the existing rules.

Bona fide residency is not paperwork — the IRS has signalled active scrutiny via the Gajwani case and CCM 202538025. The three statutory tests (183-day presence, tax-home test, closer-connection test under IRC §937 and Treas. Reg. §1.937-2), plus the Act 60 requirements (annual $10,000 charitable donation, property purchase within two years), all apply. Pre-move appreciation remains U.S.-sourced under the 10-year lookback rule.

At a Glance

EffectiveJan 1, 2027

Current0% CG / div / int

New Rate4% CG / div / int

ProgramAct 60-2019, Ch. 2

FederalIRC §933

SunsetExtended to 2055

Sources: Puerto Rico Act 38-2026; Puerto Rico DDEC; IRC §933; Holland & Knight, November 2025.

5W Action Item

For every advisor, family office, or operator with U.S.-citizen crypto-wealthy clients: identify candidates for an Act 60 application now. The decree process took an average of eight months in 2025 — meaning the practical filing window for the 0% rate is closing faster than the calendar deadline suggests.

ii.Shift 02 · The Licensing PerimeterSingapore FSMA Part 9: the offshore loophole closes.

Singapore's regulatory clarity has long been a magnet. The June 30, 2025 commencement of FSMA Part 9 sharpens that clarity — by closing the path Singapore-based crypto firms used to serve overseas customers without an MAS licence.

The Monetary Authority of Singapore brought Part 9 of the Financial Services and Markets Act 2022 into force on June 30, 2025. Under Part 9, Singapore-based Digital Token Service Providers serving only customers outside Singapore now require a DTSP licence. The previous regime — the Payment Services Act 2019 — covered services to Singaporean customers but left a gap for purely overseas-facing operations. That gap is now closed.

In its June 6, 2025 media release, MAS stated explicitly that it "will generally not issue a licence" for such structures, citing money-laundering risk and the limits of effective supervision over substantively offshore activity. Affected firms must restructure substantive operations into Singapore or cease activity. Penalties for unlicensed operation: up to SGD 250,000 and three years' imprisonment.

The signal is not anti-crypto — Singapore continues to license substantive in-jurisdiction operators and remains one of the most regulator-clear environments globally. The signal is the end of "Singapore as a flag of convenience" for overseas-only DTSPs.

At a Glance

EffectiveJun 30, 2025

StatuteFSMA 2022, Pt. 9

RegulatorMAS

ScopeOverseas-only DTSPs

PostureWill not issue

PenaltySGD 250k / 3 yrs

Source: MAS media release, June 6, 2025; Financial Services and Markets Act 2022.

5W Action Item

For any operator using a Singapore entity to serve overseas clients in DPTs or capital-markets tokens: the regulatory window for that structure has closed. Either build substantive Singapore operations and apply for licensing under PSA / FSMA / SFA, or relocate the regulated activity to a jurisdiction whose framework accommodates the structure.

iii.Shift 03 · The Federal ConsolidationUAE CMA–VARA: the framework consolidates.

The single most important regulatory expansion in crypto in 2025. The UAE has unified its federal and Dubai-emirate oversight into one mutually recognized framework — extending VARA's reach across the country and giving the UAE arguably the most fully codified crypto regime in the world.

The August 2025 cooperation agreement between the UAE's Capital Market Authority (CMA, formerly the SCA) and Dubai's Virtual Assets Regulatory Authority (VARA) establishes mutual recognition of VASP licences, joint application review processes, coordinated monitoring, and a shared enforcement framework. A VASP licensed by either authority is effectively registered to operate across the UAE.

The underlying architecture: Dubai Law No. 4 of 2022 established VARA as the world's first regulator dedicated exclusively to virtual assets. VARA's Rulebook V2.0 governs the regulated activities — exchange, custody, broker-dealer, lending, advisory, and issuance — at a level of granularity the federal framework has not yet replicated. UAE Federal Decree-Law No. 32 of 2025 and No. 33 of 2025 codify the federal layer that the CMA now oversees.

Tax architecture remains the strongest in the world for crypto-native individuals: 0% personal income tax, 0% capital gains tax, and a 2024 Federal Tax Authority clarification confirming all crypto transactions are VAT-exempt retroactively to 2018. Corporate tax is 9% on profits above AED 375,000.

At a Glance

EffectiveAug 2025

FederalCMA (former SCA)

EmirateVARA (Dubai)

FoundingDubai Law 4/2022

Personal Tax0% / 0%

Crypto VATExempt (retro 2018)

Sources: VARA (vara.ae); UAE Federal Decree-Law No. 32 / No. 33 of 2025; UAE Federal Tax Authority.

5W Action Item

For operators evaluating jurisdictions for either residence or regulated entity: the UAE proposition is now structurally stronger than it has ever been. A VARA licence in Dubai now carries federal recognition. The combination of 0% personal tax, codified VASP licensing, and the federal-emirate consolidation is the most complete proposition currently available globally.

The Convergence

Eighteen months. Three jurisdictions.

The shifts are not coordinated, but they are converging. Each represents a different government deciding — independently and on different rationales — that the era of casual jurisdictional treatment for crypto wealth is over.

None of these three governments coordinated. The drivers are independent: Singapore is closing a money-laundering exposure, the UAE is consolidating jurisdiction across emirates, Puerto Rico is rebalancing fiscal incentives against revenue. But the practical effect on every crypto-wealthy individual and operator is identical: the era of casual jurisdictional treatment is over.

The next decade of crypto wealth will be defined by structure — by which decree was filed, which licence was obtained, which Singapore-substantive operation was built before the deadline. The advisors and firms that can architect that structure for clients are about to own a market that previously didn't need them.

What It Means

Four cohorts. One window.

For Crypto Founders & Operators

Pick a jurisdiction now. Pick on architecture, not vibe.

The era of "I'll incorporate in Singapore" without a substantive presence is over. Pick the regime that fits the activity: VARA for codified exchange / custody, MAS for licensed Singapore-substantive operations, FINMA for institutional infrastructure, MFSA for EU-passporting under MiCA. The decision should be made on regulatory fit, not headline tax rate.

For Family Offices & Wealth Advisors

The 0% Puerto Rico window is a seven-month sprint.

Every U.S.-citizen client with material unrealized crypto gains needs an Act 60 assessment now. The decree process took roughly eight months in 2025 — meaning the practical filing window for the 0% rate is narrower than the calendar suggests. This is the most actionable single regulatory deadline crypto has produced.

For Exchanges & Custodians

Substantive licensing is now the default.

Singapore has closed the offshore-only DTSP route. The UAE has unified federal and emirate VASP recognition. Hong Kong's SFC regime continues to expect institutional-grade controls. The operating cost of being in this category has stepped up — and the brands that can demonstrate substantive compliance will win the institutional relationships now in motion.

For Communications & Brand

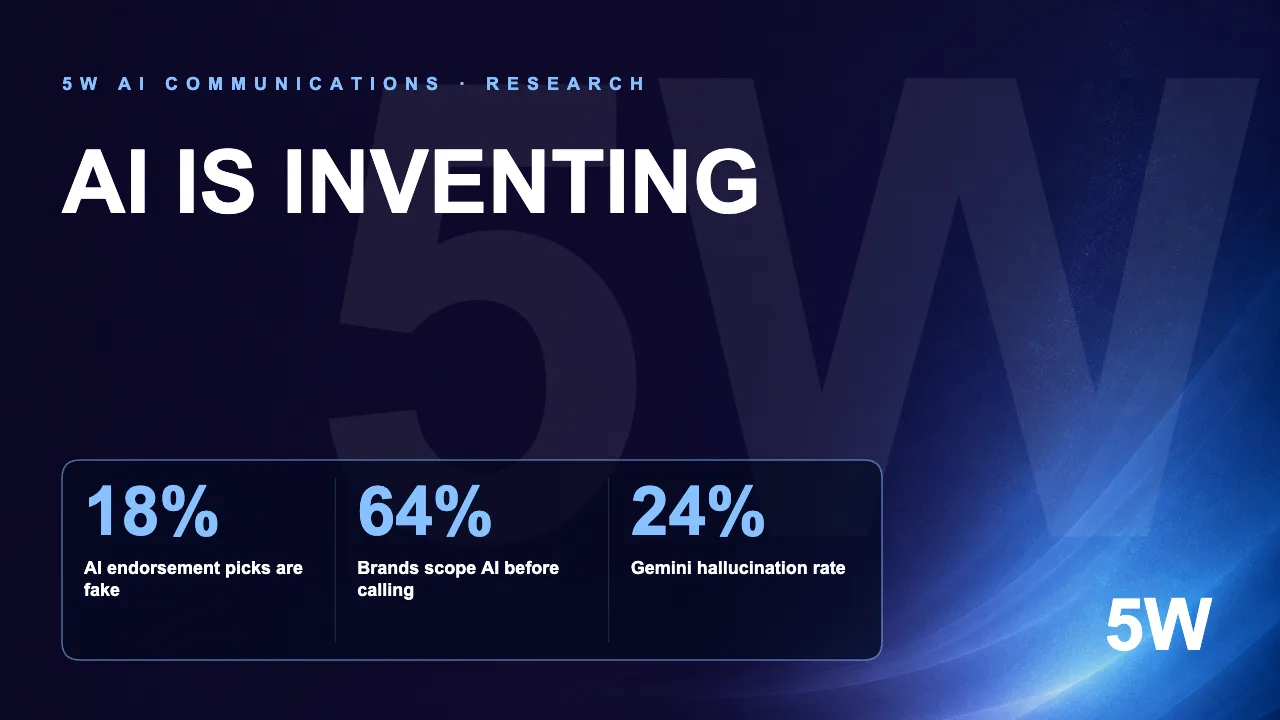

AI visibility is the new licence to be considered.

Every advisor, jurisdiction, custodian, and law firm in this window is being shortlisted inside ChatGPT, Claude, Gemini, and Perplexity — before a single phone call is placed. The brands the engines can cite are the brands in the room. Investing in AI visibility now is the cheapest version of buying entry to the conversations that will define the next decade.

On the Horizon

Three more shifts to watch in 2026–27.

The three core shifts in this brief are not the whole story. Several additional regulatory moves are tracked here as the next layer of the same map.

2026–27

U.S. GENIUS Act — stablecoin framework.

Signed into law in July 2025, the GENIUS Act establishes the first U.S. federal regulatory framework for stablecoins, including definitions, reserve requirements, and AML/CFT standards. Effective date is the later of January 18, 2027 or 120 days following final implementing regulations.

Source: U.S. Congress, GENIUS Act.In Force

EU MiCA — Markets in Crypto-Assets regulation.

Stablecoin provisions came into effect June 30, 2024; full regime applies across the EU. Notable secondary effect: Circle's EURC posted 2,727% year-over-year growth as the licensed euro-denominated stablecoin under MiCA. Malta and Portugal operate within this framework.

Source: European Parliament; Chainalysis 2025 Geography of Cryptocurrency Report.2026

Singapore stablecoin legislation & tokenized assets.

MAS confirmed at the November 2025 Singapore FinTech Festival that draft stablecoin legislation will be published in 2026. Framework prioritizes full reserve backing with high-quality liquid assets. Tokenized government bills are also being trialled using wholesale CBDC.

Source: MAS; Singapore FinTech Festival 2025.Full report

Read the PDF

Get in touch

Let's build your next chapter.

Tell us what you're working on. A senior strategist will respond within one business day.

- info@5wpr.com

- Phone

- 212.999.5585

- Offices

- New York · HQ469 7th Avenue, Floor 8

New York, NY 10018Miami100 SE 2nd Street, Floor 38

Miami, FL 33131Tampa110 South 12th Street

Tampa, FL 33602