EXECUTIVE SUMMARY

5W and Haute Wealth jointly audited how the five major generative AI engines — ChatGPT, Perplexity, Gemini, Claude, and Microsoft Copilot — answer the questions ultra-high-net-worth families actually ask: about premium financing, private placement life insurance (PPLI), irrevocable life insurance trusts (ILITs), estate liquidity, business succession, and charitable legacy planning.

The answers are confident. They are fluent. They are frequently wrong, and the way they are wrong is structural, predictable, and currently unsupervised. What follows is documentation of the specific failures — what AI engines are telling UHNW principals today, and what the correct answer is.

5W is the premier AI communications firm in the United States. This audit is the second study in our public AI Visibility research line — paired with the Invisible Tower Index (luxury real estate) — and serves as proof of concept for the AI Communications Practice.

KEY FINDINGS

- STAT 1: $15M — Permanent federal estate exemption per person (effective Jan 1, 2026) that AI engines routinely miss

- STAT 2: 5/5 — All five major AI engines under-disclose premium financing risk in their answers

- STAT 3: 66% — Share of GenAI users who have used it for financial advice

- STAT 4: 85% — Share of those users who acted on the AI's recommendation

- STAT 5: 37% — Perplexity citation hallucination rate (Columbia Journalism Review, March 2025)

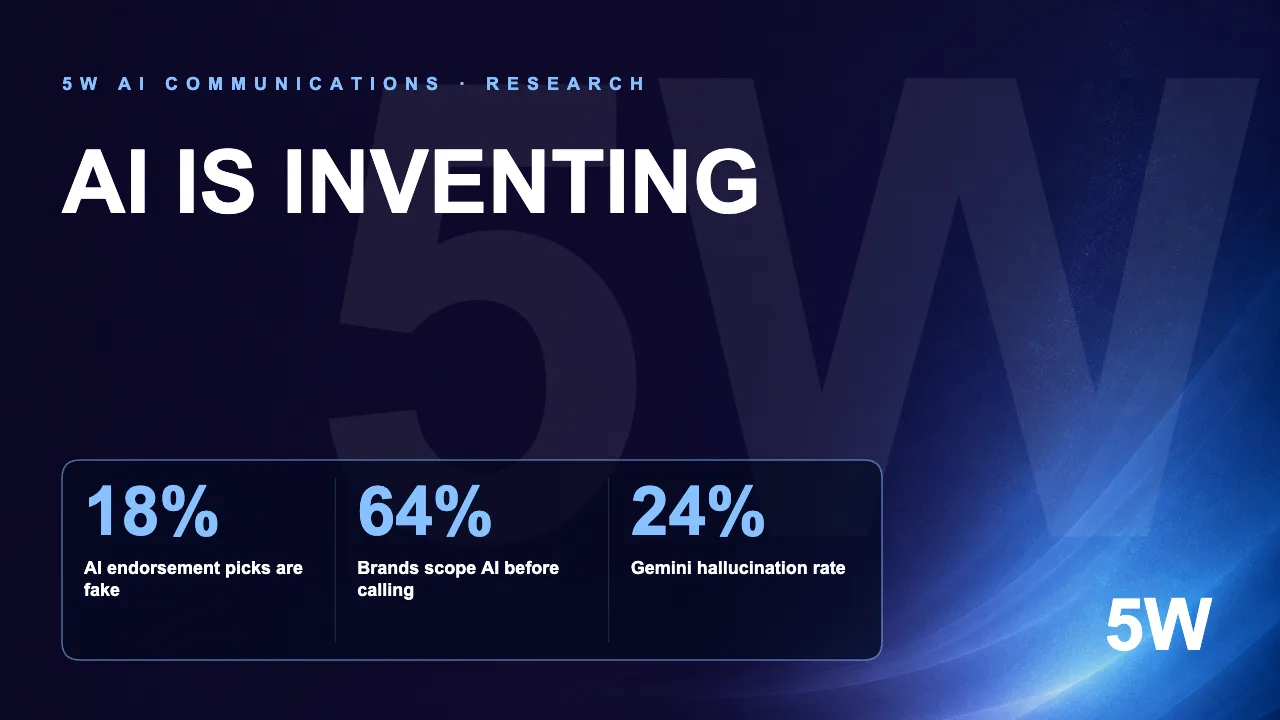

- STAT 6: 20–36% — ChatGPT-4o and Gemini Advanced financial literature hallucination rates (IJDSA, February 2025)

- STAT 7: Claude B− — Highest overall grade among the five engines audited

- STAT 8: D or lower — Boutique wealth firm visibility score across every engine reviewed

THREE ANSWERS AI IS GETTING WRONG, RIGHT NOW

MISANSWER 01 — ESTATE TAX

Q: "Should I use my federal estate exemption before it gets cut in half in 2026?"

What AI engines say: The federal estate, gift, and GST exemption is scheduled to "sunset" on January 1, 2026, reverting from roughly $14M to approximately $7M per person. Principals should act before year-end to lock in the higher exemption through gifting strategies, SLATs, and irrevocable trust funding.

What is actually true: The TCJA sunset was repealed. The One Big Beautiful Bill Act, signed July 4, 2025 (Pub. L. 119-21), permanently raised the federal estate, gift, and GST exemption to $15 million per person ($30 million per married couple) effective January 1, 2026, indexed for inflation beginning 2027. The "use it or lose it" pressure no longer exists in current law. Acting on the AI's framing means making irrevocable transfers for a tax reason that does not apply.

MISANSWER 02 — PREMIUM FINANCING

Q: "How does premium financing work, and is it right for me?"

What AI engines say: Premium financing lets high-net-worth families fund large permanent life insurance policies without disrupting their capital. It preserves liquidity, supports long-term planning, mitigates estate tax exposure on trust-owned policies, and can free up capital for other investments. Generally appropriate for individuals with significant assets seeking efficient wealth transfer.

What's missing: The five disclosed risks every reputable practitioner names — interest rate risk, collateral call risk, policy performance risk, refinancing risk, and carrier credit risk — are routinely buried, minimized, or omitted entirely. Collateral call risk, the single most consequential downside scenario, is the one most often missing. A registered representative who delivered the same answer to a client would face Reg BI exposure. The AI faces none.

MISANSWER 03 — ADVISOR SELECTION

Q: "Who are the best premium financing or PPLI firms for ultra-high-net-worth families?"

What AI engines say: A confident, neatly-formatted shortlist of large incumbents — Schwab, Fidelity, Vanguard, Northwestern Mutual, the major wirehouses — often paired with named individual advisors and firm descriptions. The shortlist looks comprehensive.

What is actually happening: The same prompt produces a different shortlist on the next run. Some named firms do not offer premium financing. Some named advisors are no longer with the firm cited. Boutique RIAs, multi-family offices, and specialist insurance practices — the firms the wealthiest 1,000 American families actually retain — are nearly entirely absent from every engine. The principal sees confidence; the engine is rolling dice.

THE VISIBILITY INDEX — WHO SHOWS UP WHEN UHNW FAMILIES ASK AI FOR AN ADVISOR

Hallucination is the headline. Visibility is the operating consequence. When an UHNW principal opens an AI engine and asks "best premium financing firms," "top PPLI advisors," or "ILIT specialists for $50M+ families," who appears in the answer determines who gets considered, vetted, and ultimately retained. Most wealth firms have no visibility data on this. None of them have a dashboard. The brand impressions that will define the next decade of the wealth industry are happening invisibly.

The pattern across every engine: a strong, structural visibility bias toward a small number of large incumbents — Schwab, Fidelity, Vanguard, Northwestern Mutual, and the wirehouses — and a near-total absence of the boutique RIAs, multi-family offices, and specialist insurance practices the wealthiest American families actually retain. The firms that win on AI visibility today are not the firms that win on AUM, brand prestige, or fiduciary quality. They are the firms whose published content the engines can read, parse, and trust.

ENGINE-BY-ENGINE RANKING — UHNW WEALTH CATEGORY

- Claude — Overall: B− | Accuracy: B+ | Risk Disclosure: B | Source Quality: B− | Boutique Visibility: D

- Perplexity — Overall: C+ | Accuracy: B | Risk Disclosure: C | Source Quality: C+ | Boutique Visibility: C

- ChatGPT — Overall: C | Accuracy: B− | Risk Disclosure: C+ | Source Quality: C | Boutique Visibility: D+

- Gemini — Overall: C | Accuracy: C+ | Risk Disclosure: C | Source Quality: C+ | Boutique Visibility: D

- Copilot — Overall: C− | Accuracy: C | Risk Disclosure: C− | Source Quality: C | Boutique Visibility: D−

Grades reflect 5W's assessment of publicly documented engine behavior on UHNW wealth queries against the published positions of FINRA, the SEC, the NAIC, the IRS, and major fiduciary trade bodies. Methodology details are provided below.

WHAT WINS INSIDE THE ENGINES

Three signals correlate with appearing in the answer: a strong .com domain history with regulator citations or original research, a clear topical authority signal in canonical sources (Wikipedia, Investopedia, mainstream business press), and recent original content with named human authors. None of these are paid placements. None of them are accidents.

What loses: pure social-channel presence (a firm with a strong Instagram and no canonical-source footprint is invisible), generic SEO content (engines have learned to discount it), and gated thought leadership AI crawlers cannot access (PDFs behind email walls do not exist, from the engine's perspective).

The wealth firms that will win the next ten years are not the ones with the biggest brand spend or the most polished pitch decks. They are the ones with verifiable, original, regulator-aligned content under their own canonical domain — content an AI engine can read, cite, and trust. The visibility battle is being fought at the level of crawled, indexed, schema-tagged pages. Most UHNW firms are still fighting it at the level of glossy brochures.

THE HALLUCINATION FINDINGS — FIVE WAYS AI IS GETTING WEALTH ADVICE WRONG

Beyond the three concrete misanswers above, the audit identified five repeating failure patterns across every engine reviewed. Findings were validated against published regulator guidance from FINRA's 2026 Annual Regulatory Oversight Report, IRS publications post-OBBBA, NAIC bulletins, and peer-reviewed AI hallucination research.

FINDING I — THE TAX LAW THAT ISN'T THERE ANYMORE

The most important estate tax change in a decade is the One Big Beautiful Bill Act, signed July 4, 2025. It eliminated the TCJA sunset and permanently raised the federal estate, gift, and GST tax exemption to $15 million per person — $30 million per married couple — effective January 1, 2026, indexed for inflation beginning 2027.

This is not a footnote. It is the foundational fact every premium financing illustration, every ILIT funding decision, every SLAT recommendation, and every "use it or lose it" gifting conversation between July 2025 and now has had to be rebuilt around. AI engines drawing on training corpora saturated with pre-OBBBA advisor content continue to surface the obsolete sunset narrative as if it were live planning advice. The structural cause is well documented: models hallucinate financial data more often than other categories because their training corpora are saturated with the prior version of the truth. The model's prior is louder than the update.

FINDING II — THE MISSING RISK DISCLOSURES

Premium financing is a sophisticated, suitable-for-some strategy that comes with five well-known risks: interest cost and rate risk, collateral call risk, policy performance risk, refinancing risk, and carrier credit risk. Every reputable practitioner names each of these explicitly. AI engines do not. The modal answer leads with the upside and treats the risk catalog as an afterthought. Collateral call risk — the single most important downside scenario — is regularly omitted entirely. This is exactly the regulatory failure mode FINRA flagged: AI-generated communications with retail customers that fail to be "fair, balanced, and compliant."

FINDING III — THE CITATION QUALITY COLLAPSE

When an AI engine cites a source on an UHNW wealth question, what surfaces is rarely regulators (.gov), the IRS, or major fiduciary trade bodies (ACTEC, AALU, AICPA PFP, Society of FSP). What surfaces is content-marketing material from advisors trying to rank in Google — SEO blog posts, captive carrier explainer pages, and aggregator sites whose business model is lead capture, not accuracy.

A March 2025 Columbia Journalism Review study found that Perplexity, despite being the most "citation-forward" of the major engines, hallucinated citations at a 37% rate — meaning more than one in three citations contained fabricated or misattributed claims. A separate February 2025 peer-reviewed analysis in the International Journal of Data Science and Analytics tested ChatGPT-4o, o1-preview, and Gemini Advanced on financial literature citations and documented hallucination rates between 20% and 36% across the three engines. The principal sees a footnote and assumes due diligence. None has occurred.

FINDING IV — THE CONSISTENCY PROBLEM

The same prompt, run on the same engine, on the same day, returns materially different answers. This is the temperature parameter doing what it is designed to do. For an UHNW principal building a shortlist of advisors, structuring a trust, or evaluating a carrier, the consequence is that the answer they got is one of many answers they could have gotten — and they have no way of knowing how representative it is. The principal sees a confident, neatly formatted answer and assumes it represents the considered judgment of the engine. It represents one roll of the dice.

FINDING V — THE QUESTION AI NEVER ASKS BACK

The single biggest gap between an AI engine and a competent human fiduciary is not the answer — it is the follow-up. A human advisor responding to "should I do premium financing?" asks: Is the policy in trust? What is your liquidity profile? What are your other estate liquidity sources? What is your view on rates? Have you stress-tested the carrier? Who is the trustee? What does your existing irrevocable structure look like?

The AI engine does not ask any of these. It answers. As MIT's Andrew Lo has noted, the most concerning thing about large language models is that no matter what you ask, they always come back with an answer that sounds authoritative — even if it's not. For a $50,000 question, that's friction. For a $50 million question, it's a disaster waiting to happen.

"The wealth industry has spent two years debating whether AI is a threat or an opportunity. The audit data is clear: it is both, and the firms acting like it's neither are the ones losing the next decade." — 5W AI Communications Practice

IMPLICATIONS

FOR UHNW PRINCIPALS AND FAMILY OFFICES

Treat any AI answer on tax, estate, insurance, or trust matters as a starting point for a question, not as advice. Cross-check every cited fact against current law as of 2026. Assume the engine does not know about the OBBBA exemption change unless it explicitly cites it. Never act on AI-generated wealth advice without a credentialed fiduciary in the loop. The cost of being wrong is asymmetric — the upside of an AI-derived shortcut is hours saved; the downside is a seven-figure tax error or an irrevocable structure built on the wrong foundation.

FOR WEALTH ADVISORS AND FIRMS

Audit your AI visibility now. If your firm does not appear when an UHNW principal asks an AI engine about your specialty, you are losing the most consequential brand impressions of the next decade — silently, with no analytics dashboard telling you. Audit your published content for technical accuracy against current law. Move gated, PDF-locked thought leadership onto open, crawled, schema-marked HTML pages. Name your authors. Cite your sources. The engines reward exactly what regulators reward — and the firms still treating this as an SEO afterthought are the ones invisible inside the answers.

FOR REGULATORS

FINRA's 2026 Annual Regulatory Oversight Report took the right first step by naming hallucination as a supervisory concern. The harder question is consumer-facing: what is the disclosure obligation when a retail-grade AI engine answers a regulated-product question without the disclosures a registered representative would be required to provide? The current answer is none — and that is the gap the next round of rulemaking will need to close.

FROM THE PUBLISHERS

"AI is now the silent advisor in the room when ultra-high-net-worth families make their most important decisions. That is a risk no fiduciary, no family principal, and no regulator can ignore. Haute Wealth was built on the conviction that real wealth planning is a human act — and this audit makes the cost of forgetting that visible."

— Kamal Hotchandani, Founder & CEO, Haute Media Group; Founder, Haute Wealth

"AI has changed every part of how decisions get made in the world. Where to eat, who to hire, what doctor to see, what advisor to trust — the answer used to come from a person. Now it comes from a chatbot, and people act on it. This is the biggest shift in information authority in a century, happening with no rules, no auditor, and no firm knowing what is being said about them inside the engines. Wealth is one of the first places it gets expensive. Every industry is next."

— Ronn Torossian, Founder & Chairman, 5W

WHERE HAUTE WEALTH FITS

Haute Wealth launched in April 2025 as the wealth-planning vertical of Haute Media Group, founded by Kamal Hotchandani, with a mandate to bring institutional-quality life insurance, premium financing, PPLI, and estate liquidity strategy to ultra-high-net-worth families on a fiduciary, white-glove model. The firm's published content — including its premium financing brief — is one of the few public UHNW-focused educational resources in the category that names the full risk catalog explicitly. That is exactly the kind of content AI engines are increasingly weighting as authoritative source material. It is also exactly the kind of content most of Haute Wealth's competitors are not producing.

REQUEST AN AI VISIBILITY DIAGNOSTIC

5W's AI Communications Practice offers a free 30-minute diagnostic call — running live queries on your firm across five AI engines, scored on the same 25-point rubric used in this audit. Most firms discover they score under 12 of 25. Some score under 6. The diagnostic is the starting point.

For wealth firms, RIAs, family offices, and specialist insurance practices ready to audit their AI visibility: research@5wpr.com or media@5wpr.com.